Page 68 - 2board23full

P. 68

Financial Statements

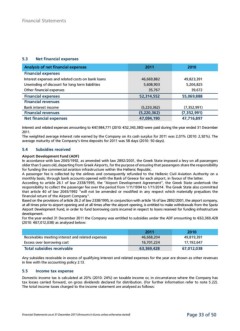

5.3 Net financial expenses 2011 2010

Analysis of net financial expenses 46,669,882 49,823,391

Financial expenses 5,608,903 5,206,825

35,767 39,672

Interest expenses and related costs on bank loans

Unwinding of discount for long term liabilities 52,314,552 55,069,888

Other financial expenses

(5,220,362) (7,352,991)

Financial expenses

Financial revenues (5,220,362) (7,352,991)

47,094,190 47,716,897

Bank interest income

Financial revenues

Net financial expenses

Interest and related expenses amounting to €47,984,771 (2010: €52,343,380) were paid during the year ended 31 December

2011.

The weighted average interest rate earned by the Company on its cash surplus for 2011 was 2,01% (2010: 2,92%). The

average maturity of the Company’s time deposits for 2011 was 58 days (2010: 50 days).

5.4 Subsidies received

Airport Development Fund (ADF)

In accordance with law 2065/1992, as amended with law 2892/2001, the Greek State imposed a levy on all passengers

older than 5 years old, departing from Greek Airports, for the purpose of ensuring that passengers share the responsibility

for funding the commercial aviation infrastructure within the Hellenic Republic.

A passenger fee is collected by the airlines and consequently refunded to the Hellenic Civil Aviation Authority on a

monthly basis, through bank accounts opened with the Bank of Greece for each airport, in favour of the latter.

According to article 26.1 of law 2338/1995, the “Airport Development Agreement”, the Greek State undertook the

responsibility to collect the passenger fee over the period from 1/11/1994 to 1/11/2014. The Greek State also committed

that article 40 of law 2065/1992 “will not be amended or modified in any respect which materially prejudices the

financial return of the Airport Company”.

Based on the provisions of article 26.2 of law 2338/1995, in conjunction with article 16 of law 2892/2001, the airport company,

at all times prior to airport opening and at all times after the airport opening, is entitled to make withdrawals from the Spata

Airport Development Fund, in order to fund borrowing costs incurred in respect to loans received for funding infrastructure

development.

For the year ended 31 December 2011 the Company was entitled to subsidies under the ADF amounting to €63,369,428

(2010: €67,012,038) as analysed below:

2011 2010

Receivables meeting interest and related expenses 46,668,204 49,819,391

Excess over borrowing cost 16,701,224 17,192,647

Total subsidies receivable 63,369,428 67,012,038

Any subsidies receivable in excess of qualifying interest and related expenses for the year are shown as other revenues

in line with the accounting policy 2.13.

5.5 Income tax expense

Domestic income tax is calculated at 20% (2010: 24%) on taxable income or, in circumstance where the Company has

tax losses carried forward, on gross dividends declared for distribution. (For further information refer to note 5.22).

The total income taxes charged to the income statement are analysed as follows:

Financial Statements as at 31 December 2011 (Amounts in Euros unless otherwise stated) Page 33 of 50

5.3 Net financial expenses 2011 2010

Analysis of net financial expenses 46,669,882 49,823,391

Financial expenses 5,608,903 5,206,825

35,767 39,672

Interest expenses and related costs on bank loans

Unwinding of discount for long term liabilities 52,314,552 55,069,888

Other financial expenses

(5,220,362) (7,352,991)

Financial expenses

Financial revenues (5,220,362) (7,352,991)

47,094,190 47,716,897

Bank interest income

Financial revenues

Net financial expenses

Interest and related expenses amounting to €47,984,771 (2010: €52,343,380) were paid during the year ended 31 December

2011.

The weighted average interest rate earned by the Company on its cash surplus for 2011 was 2,01% (2010: 2,92%). The

average maturity of the Company’s time deposits for 2011 was 58 days (2010: 50 days).

5.4 Subsidies received

Airport Development Fund (ADF)

In accordance with law 2065/1992, as amended with law 2892/2001, the Greek State imposed a levy on all passengers

older than 5 years old, departing from Greek Airports, for the purpose of ensuring that passengers share the responsibility

for funding the commercial aviation infrastructure within the Hellenic Republic.

A passenger fee is collected by the airlines and consequently refunded to the Hellenic Civil Aviation Authority on a

monthly basis, through bank accounts opened with the Bank of Greece for each airport, in favour of the latter.

According to article 26.1 of law 2338/1995, the “Airport Development Agreement”, the Greek State undertook the

responsibility to collect the passenger fee over the period from 1/11/1994 to 1/11/2014. The Greek State also committed

that article 40 of law 2065/1992 “will not be amended or modified in any respect which materially prejudices the

financial return of the Airport Company”.

Based on the provisions of article 26.2 of law 2338/1995, in conjunction with article 16 of law 2892/2001, the airport company,

at all times prior to airport opening and at all times after the airport opening, is entitled to make withdrawals from the Spata

Airport Development Fund, in order to fund borrowing costs incurred in respect to loans received for funding infrastructure

development.

For the year ended 31 December 2011 the Company was entitled to subsidies under the ADF amounting to €63,369,428

(2010: €67,012,038) as analysed below:

2011 2010

Receivables meeting interest and related expenses 46,668,204 49,819,391

Excess over borrowing cost 16,701,224 17,192,647

Total subsidies receivable 63,369,428 67,012,038

Any subsidies receivable in excess of qualifying interest and related expenses for the year are shown as other revenues

in line with the accounting policy 2.13.

5.5 Income tax expense

Domestic income tax is calculated at 20% (2010: 24%) on taxable income or, in circumstance where the Company has

tax losses carried forward, on gross dividends declared for distribution. (For further information refer to note 5.22).

The total income taxes charged to the income statement are analysed as follows:

Financial Statements as at 31 December 2011 (Amounts in Euros unless otherwise stated) Page 33 of 50