Page 100 - Annual_Report_2016

P. 100

Financial Statements aia.gr

The Company as a lessor

Refer to note 5.1.

5.28 Commitments

As at 31 December 2016 the Company has the following significant commitments:

a) Capital expenditure commitments amounting to approximately €13.4m (2015: €6.5m)

b) Operating service commitments, which are estimated to be approximately to €101.0m (2015: €121.4m)

mainly related to security, maintenance, fire protection, transportation, parking and cleaning services, to

be settled as follows:

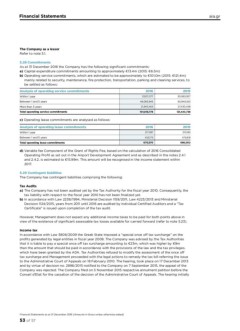

Analysis of operating service commitments 2016 2015

Within 1 year 33,011,377 30,063,927

Between 1 and 5 years 46,063,946 63,949,353

More than 5 years 21,943,455 27,430,458

Total operating service commitments 101,018,778 121,443,738

c) Operating lease commitments are analysed as follows: 2016 2015

Analysis of operating lease commitments 217,397 210,183

453,173 475,818

Within 1 year 670,570 686,002

Between 1 and 5 years

Total operating lease commitments

d) Variable fee Component of the Grant of Rights Fee, based on the calculation of 2016 Consolidated

Operating Profit as set out in the Airport Development Agreement and as described in the notes 2.4.1

and 2.4.2, is estimated to €15.99m. This amount will be recognised in the income statement within

2017.

5.29 Contingent liabilities

The Company has contingent liabilities comprising the following:

Tax Audits

a) The Company has not been audited yet by the Tax Authority for the fiscal year 2010. Consequently, the

tax liability with respect to the fiscal year 2010 has not been finalized yet.

b) In accordance with Law 2238/1994, Ministerial Decision 1159/2011, Law 4223/2013 and Ministerial

Decision 1124/2015, years from 2011 until 2016 are audited by individual Certified Auditors and a “Tax

Certificate” is issued upon completion of the tax audit.

However, Management does not expect any additional income taxes to be paid for both points above in

view of the existence of significant assessable tax losses available for carried forward (refer to note 5.23).

Income tax

In accordance with Law 3808/2009 the Greek State imposed a “special once off tax surcharge” on the

profits generated by legal entities in fiscal year 2008. The Company was advised by the Tax Authorities

that it is liable to pay a special once off tax surcharge amounting to €23m, which was higher by €9m

than the amount that should be paid in accordance with the provisions of the law and the tax privileges,

which have been granted by the ADA. Tax Authorities refused to modify the assessment of the once off

tax surcharge and Management proceeded with the legal actions to remedy the tax bill referring the issue

to the Administrative Court of Appeals on 18 February 2010. The hearing, took place on 17 December 2013

and by virtue of decision no. 2896/2015 notified to the Company on 7 September 2015, the appeal of the

Company was rejected. The Company filed on 5 November 2015 respective annulment petition before the

Conseil d’Etat for the cassation of the decision of the Administrative Court of Appeals. The hearing initially

Financial Statements as at 31 December 2016 (Amounts in Euros unless otherwise stated)

53 of 57

The Company as a lessor

Refer to note 5.1.

5.28 Commitments

As at 31 December 2016 the Company has the following significant commitments:

a) Capital expenditure commitments amounting to approximately €13.4m (2015: €6.5m)

b) Operating service commitments, which are estimated to be approximately to €101.0m (2015: €121.4m)

mainly related to security, maintenance, fire protection, transportation, parking and cleaning services, to

be settled as follows:

Analysis of operating service commitments 2016 2015

Within 1 year 33,011,377 30,063,927

Between 1 and 5 years 46,063,946 63,949,353

More than 5 years 21,943,455 27,430,458

Total operating service commitments 101,018,778 121,443,738

c) Operating lease commitments are analysed as follows: 2016 2015

Analysis of operating lease commitments 217,397 210,183

453,173 475,818

Within 1 year 670,570 686,002

Between 1 and 5 years

Total operating lease commitments

d) Variable fee Component of the Grant of Rights Fee, based on the calculation of 2016 Consolidated

Operating Profit as set out in the Airport Development Agreement and as described in the notes 2.4.1

and 2.4.2, is estimated to €15.99m. This amount will be recognised in the income statement within

2017.

5.29 Contingent liabilities

The Company has contingent liabilities comprising the following:

Tax Audits

a) The Company has not been audited yet by the Tax Authority for the fiscal year 2010. Consequently, the

tax liability with respect to the fiscal year 2010 has not been finalized yet.

b) In accordance with Law 2238/1994, Ministerial Decision 1159/2011, Law 4223/2013 and Ministerial

Decision 1124/2015, years from 2011 until 2016 are audited by individual Certified Auditors and a “Tax

Certificate” is issued upon completion of the tax audit.

However, Management does not expect any additional income taxes to be paid for both points above in

view of the existence of significant assessable tax losses available for carried forward (refer to note 5.23).

Income tax

In accordance with Law 3808/2009 the Greek State imposed a “special once off tax surcharge” on the

profits generated by legal entities in fiscal year 2008. The Company was advised by the Tax Authorities

that it is liable to pay a special once off tax surcharge amounting to €23m, which was higher by €9m

than the amount that should be paid in accordance with the provisions of the law and the tax privileges,

which have been granted by the ADA. Tax Authorities refused to modify the assessment of the once off

tax surcharge and Management proceeded with the legal actions to remedy the tax bill referring the issue

to the Administrative Court of Appeals on 18 February 2010. The hearing, took place on 17 December 2013

and by virtue of decision no. 2896/2015 notified to the Company on 7 September 2015, the appeal of the

Company was rejected. The Company filed on 5 November 2015 respective annulment petition before the

Conseil d’Etat for the cassation of the decision of the Administrative Court of Appeals. The hearing initially

Financial Statements as at 31 December 2016 (Amounts in Euros unless otherwise stated)

53 of 57