Page 65 - 2board23full

P. 65

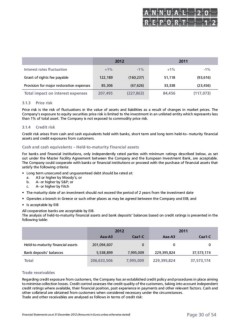

2012 2011

Interest rates fluctuation +1% -1% +1% -1%

Grant of rights fee payable 51,118 (93,616)

Provision for major restoration expenses 122,189 (160,237) 33,338 (23,456)

Total impact on interest expenses 85,306 (67,626) 84,456 (117,073)

207,495 (227,863)

3.1.3 Price risk

Price risk is the risk of fluctuations in the value of assets and liabilities as a result of changes in market prices. The

Company’s exposure to equity securities price risk is limited to the investment in an unlisted entity which represents less

than 1% of total asset. The Company is not exposed to commodity price risk.

3.1.4 Credit risk

Credit risk arises from cash and cash equivalents held with banks, short term and long term held-to- maturity financial

assets and credit exposures from customers.

Cash and cash equivalents – Held-to-maturity financial assets

For banks and financial institutions, only independently rated parties with minimum ratings described below, as set

out under the Master Facility Agreement between the Company and the European Investment Bank, are acceptable.

The Company could cooperate with banks or financial institutions or proceed with the purchase of financial assets that

satisfy the following criteria:

• Long term unsecured and unguaranteed debt should be rated at:

a. A3 or higher by Moody’s; or

b. A- or higher by S&P; or

c. A- or higher by Fitch

• The maturity date of an investment should not exceed the period of 2 years from the investment date

• Operates a branch in Greece or such other places as may be agreed between the Company and EIB; and

• Is acceptable by EIB

All cooperation banks are acceptable by EIB.

The analysis of held-to-maturity financial assets and bank deposits’ balances based on credit ratings is presented in the

following table:

2012 Caa1-C 2011 Caa1-C

Aaa-A3 Aaa-A3

Held-to-maturity financial assets 201,094,607 0 0 0

Bank deposits' balances 5,538,899 7,995,009 229,395,824 37,573,174

Total 206,633,506 7,995,009 229,395,824 37,573,174

Trade receivables

Regarding credit exposure from customers, the Company has an established credit policy and procedures in place aiming

to minimise collection losses. Credit control assesses the credit quality of the customers, taking into account independent

credit ratings where available, their financial position, past experience in payments and other relevant factors. Cash and

other collateral are obtained from customers when considered necessary under the circumstances.

Trade and other receivables are analysed as follows in terms of credit risk:

Financial Statements as at 31 December 2012 (Amounts in Euros unless otherwise stated) Page 30 of 54

Interest rates fluctuation +1% -1% +1% -1%

Grant of rights fee payable 51,118 (93,616)

Provision for major restoration expenses 122,189 (160,237) 33,338 (23,456)

Total impact on interest expenses 85,306 (67,626) 84,456 (117,073)

207,495 (227,863)

3.1.3 Price risk

Price risk is the risk of fluctuations in the value of assets and liabilities as a result of changes in market prices. The

Company’s exposure to equity securities price risk is limited to the investment in an unlisted entity which represents less

than 1% of total asset. The Company is not exposed to commodity price risk.

3.1.4 Credit risk

Credit risk arises from cash and cash equivalents held with banks, short term and long term held-to- maturity financial

assets and credit exposures from customers.

Cash and cash equivalents – Held-to-maturity financial assets

For banks and financial institutions, only independently rated parties with minimum ratings described below, as set

out under the Master Facility Agreement between the Company and the European Investment Bank, are acceptable.

The Company could cooperate with banks or financial institutions or proceed with the purchase of financial assets that

satisfy the following criteria:

• Long term unsecured and unguaranteed debt should be rated at:

a. A3 or higher by Moody’s; or

b. A- or higher by S&P; or

c. A- or higher by Fitch

• The maturity date of an investment should not exceed the period of 2 years from the investment date

• Operates a branch in Greece or such other places as may be agreed between the Company and EIB; and

• Is acceptable by EIB

All cooperation banks are acceptable by EIB.

The analysis of held-to-maturity financial assets and bank deposits’ balances based on credit ratings is presented in the

following table:

2012 Caa1-C 2011 Caa1-C

Aaa-A3 Aaa-A3

Held-to-maturity financial assets 201,094,607 0 0 0

Bank deposits' balances 5,538,899 7,995,009 229,395,824 37,573,174

Total 206,633,506 7,995,009 229,395,824 37,573,174

Trade receivables

Regarding credit exposure from customers, the Company has an established credit policy and procedures in place aiming

to minimise collection losses. Credit control assesses the credit quality of the customers, taking into account independent

credit ratings where available, their financial position, past experience in payments and other relevant factors. Cash and

other collateral are obtained from customers when considered necessary under the circumstances.

Trade and other receivables are analysed as follows in terms of credit risk:

Financial Statements as at 31 December 2012 (Amounts in Euros unless otherwise stated) Page 30 of 54